737MAX is once again in the news, only this time not for what it isn’t doing. On December 23 of last year, the same day Dennis Muilenberg resigned, Boeing announced it would shut down production of the 737MAX in January and told suppliers to stop parts shipments for a month. On January 10 of this year, Spirit Aerosystems, manufacturer of MAX fuselages announced it would lay off 2,800 workers – about a quarter of its Wichita work force (half of Spirit’s revenues come from the 737). Since then, subtier suppliers in the US and particularly Seattle and Wichita have also begun laying off workers. Boeing, however, is not laying off any workers but is redeploying them, choosing to retain valuable assembly workers for the future restart of production. Boeing announced on January 21 that it expects the MAX will be returned to service in the “middle of 2020”. Furthermore, in comments the following day, new CEO Dave Calhoun said they plan to restart MAX production “months before” the aircraft is recertified. His comments suggest production will be paused until March before restarting.

To be clear, return to service means the aircraft has been recertified by the regulators and can be safely flown. It also means that Boeing will be able to resume shipping aircraft. However, that does not mean that the aircraft already built will be flying right away. That will only happen once the aircraft already built (whether delivered to customers or not) have undergone the prescribed fixes (e.g., software updates), pilots complete training (recall that MAX simulators are in short supply) and the airlines induct them into their flight schedules. For additional clarity, “production” in the rest of this piece refers to MAX aircraft completed by Boeing. Delivery refers to MAX aircraft delivered to its customers.

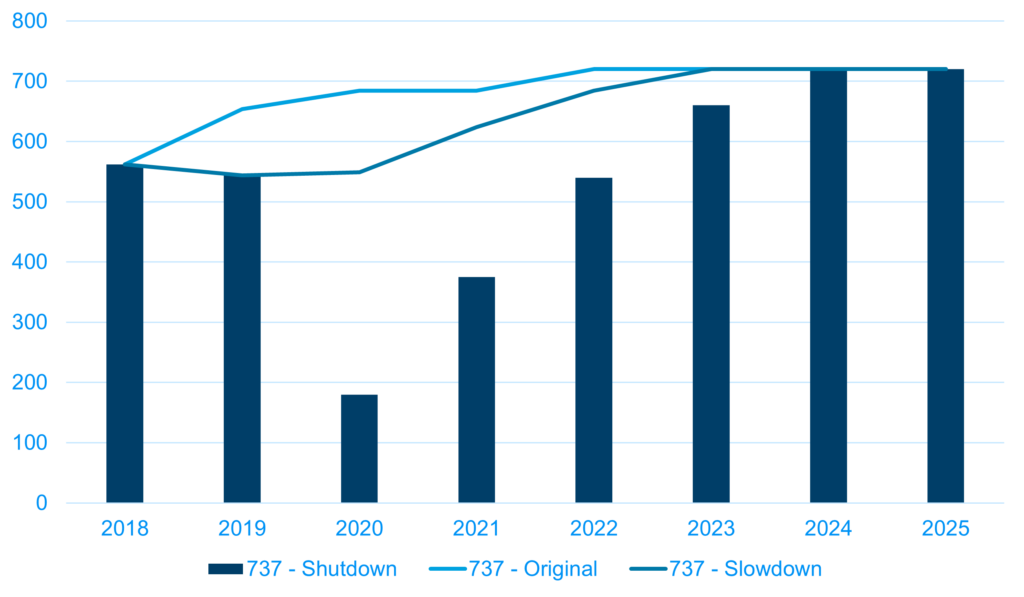

Piecing together the latest news with our understanding of what it will take to realign the supply chain to resume production, our revised build forecast is shown in the chart at left. Our understanding is MAX production is coming to a full stop no later than the end of January. We see production by Boeing resuming in April (supply of components would be started earlier than this) at an initial rate of 20-25 aircraft per month and continuing at that rate through the end of 2020. Thereafter, we estimate production will rise in 7.5 aircraft per month increments every six months until rate reaches ~42/month in early 2022. At this point, production increase increments slow to 5/month every six months, until production rises to 60/month starting in early 2024.

Note that MAX deliveries will exceed MAX production because Boeing has 400 aircraft already built. Timing for recertification, fixes to existing aircraft, pilot training, and deliveries to customers all are unknown at this time.

Low. Strictly speaking, middle of the year is June 30 / July 1. However, middle of the year can plausibly be expanded to include anytime in June or July. August is stretching it; September is out of bounds. Given that fixes have been submitted and even accounting for additional regulatory scrutiny, it seems likely the aircraft will be cleared to return to service by the end of July, if not sooner. Furthermore, the longer it takes to recertify, the more likely it will be a joint FAA-EASA recertification, reopening the majority of the regions taking delivery of the airplane.

Low for Boeing but rising to moderate for their major aerostructures subtier, Spirit Aerosystems, and the rest of the subtier supply base.

Boeing has had a supply pipeline feeding a 42/month rate (actual achieved rate was probably 39/month) after the MAX rate reduction so there is material in the pipeline to support at 20-25 aircraft per month restart. Furthermore, they are not furloughing their workers so they’ll retain more of them for the restart.

By contrast, Spirit’s position is very different. Spirit had been producing 737MAX fuselages ahead of Boeing’s 42/month rate (nominally at 52/month but actually slightly lower) and they stated they have over 100 fuselages ready to ship. So, Spirit has even more inventory from which it can ship to Boeing. Furthermore, their layoff indicates they are expecting a pause (or a significant rate reduction) to last greater than two months for their production. We don’t think they can afford to pause altogether without having significant supply chain disruptions in the future so have assumed they’ll reduce fuselage production to Boeing’s 20-25/month rate but will continue to build at that lower rate for longer, supplying the difference between that rate and the rising Boeing rate in future years from their inventory of completed fuselages. At the 737MAX build rates we forecast, their backlog of fuselages will be consumed by mid-late 2021 so they’ll have to ramp up fuselage production in mid-2021. The 2,800 employees that are being laid off now will need to find other jobs. Considering the number of aerospace related layoffs in Wichita, this is likely to take a number of them to work outside the aerospace industry and the region between now and the middle of 2021. In fact, Spirit is hosting job fairs to help their laid off employees find new employment. Spirit will face a challenge hiring and training a significant portion of the workforce needed to support 2022 and beyond build rates. There’s definitely opportunity for schedule slips in this context.

Tier 2 and 3 manufacturers also face challenges. Many suppliers added significant resource to grow their MAX related operations to keep pace with ~50 per month and largely kept them engaged at the 40-50 range throughout 2019. However, as devastating as Spirit’s reduction in force is for that Tier 1 (15% of total workers), a rate cut to half the pre-shutdown rate is going to put a significant strain on some key subtier suppliers who do not have the same scale to absorb the loss in revenue. Many of them are highly dependent on Boeing programs, whether they are selling to Boeing, Spirit, or other suppliers. Many of them have discounted their prices in response to Boeing’s Partnership for Success program and don’t have the means to keep people on the payroll throughout the pause. As we’ve said above, we think the Spirit rate reduction will be significant and last 12-15 months before they ramp up supply again, so many of their subtier suppliers will have to lay off people. This will expand the rehire and retrain challenge we noted above. Furthermore, some of the subtier suppliers will ask themselves why endure the rate reduction only to face future cost reduction pressures when high rates resume? The current crisis may be the trigger for some firms to exit aerospace altogether.

The story for engines may be more muted. Based on the above 737MAX build rates, CFM56 and LEAP production drops should mirror that of the MAX production curve. However, the initial reaction of the engine maker is far less severe than that of aerostructures suppliers. In response to the Boeing shutdown announcement, GE Aviation announced on January 13 that is would reduce 70 temporary jobs at a plant in Canada that makes LEAP 1B as well as other engines. A small cut in contrast to Spirit’s 2,800 worker layoff. One reason for this is the similar LEAP 1A powers the A320 and it is still ramping. Secondly, unlike Spirit, GE is not starting with a substantial inventory of engines built ahead of the aircraft. Indeed, LEAP engine production has probably paced growth of the overall MAX production rate. Falling MAX rates are partially offset by growing A320 rates and GE may be able to softly adjust production labor through actions like not replacing workers who leave. However, stumbles in other parts of the supply chain could impact aircraft realized production rates and therefore impact the engine maker as well.

We expect the impact to be different for different suppliers, but particularly hard on aerostructures subtiers. They will have short-term challenges to adjust to what we project will be sharply lower MAX production rates. This, in turn, will challenge the ability of the supply chain to resume build rates at the 40-50 aircraft per month level down the road.

Authoritative Actionable

Consulting in Aerospace

Sign up for our newsletter today!